Procurement fraud has been a longstanding risk for both private businesses and government agencies. This type of fraud can cost organizations huge sums of money in inflated fees, subpar materials, and more.

A recent procurement fraud investigation of a manufacturing company with operations throughout Asia uncovered losses worth over $1 billion. And according to PwC's 2024 Global Economic Crime Survey, procurement fraud ranks among the top three most disruptive economic crimes experienced by companies globally in the two previous years, just behind cybercrime and corruption.

Emerging markets are at particularly high risk for procurement fraud schemes, but businesses and governments around the world need to be vigilant. The schemes are varied, often layered, and frequently hidden in plain sight within the normal flow of contracts, invoices, and vendor relationships.

This article covers the basics of procurement fraud: what it is, what procurement fraud schemes look like, and common red flags. We also look at how graph technology can help analysts detect and investigate a procurement fraud scheme.

Procurement fraud is the manipulation of a procurement process for financial gain. In a typical scenario, a vendor is engaged for a contract above the market price in exchange for a kickback in the form of cash, material goods, or other benefits for the employee awarding the contract. It also includes manipulation of the bidding process among vendors, and schemes that only emerge after a contract has been awarded, such as a supplier delivering subpar materials while billing for something better.

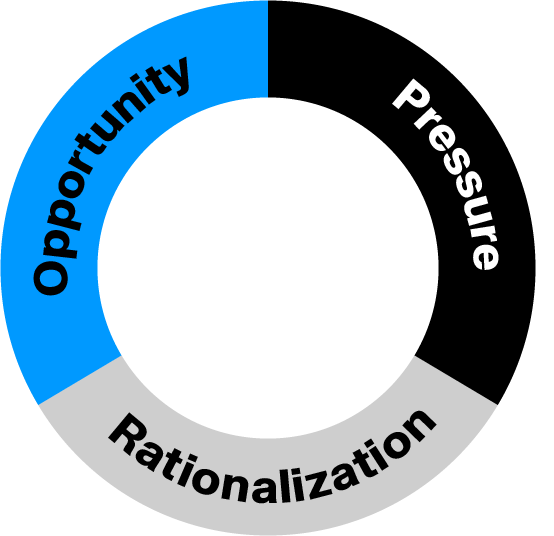

Understanding why procurement fraud happens is just as useful as knowing what it looks like. Criminologist Donald Cressey identified three conditions that tend to be present when fraud occurs, a framework later formalized by the ACFE as the Fraud Triangle: a perceived financial pressure driving the motivation to act, a perceived opportunity arising from weak controls or limited oversight, and a rationalization process through which the individual justifies the behavior to themselves.

In procurement contexts, opportunity is often the most controllable factor. Strong controls, clear segregation of duties, and connected data visibility are all foundational elements of fraud risk management, and they directly reduce the window in which procurement fraud can go undetected.

Bad actors have many ways of carrying out procurement fraud, and the schemes don't all follow the same pattern. Some occur before a contract is awarded, targeting the bidding and vendor selection process. Others only emerge after a contract is in place, when a supplier begins cutting corners or manipulating delivery. In more complex cases, multiple types of fraud run simultaneously across both stages. Here are the most common ones.

Employee contractor collusion and bribery is one of the most straightforward forms of vendor fraud: an employee responsible for the procurement process favors one vendor over another, or awards a contract above market price, in exchange for kickback money, goods, or services. The vendor gets the contract, the employee gets the reward, and the organization absorbs the loss.

Conflict of interest in a procurement process occurs when a vendor is selected based on a personal relationship rather than objective criteria. For example, the procurement manager awards a contract to a friend or family member without disclosing the connection. They may do this as a personal favor or in exchange for a material reward.

A bid rigging scheme involves collusion between vendors who manipulate the bids a business or government agency receives. Contractors may coordinate to offer identical prices, take turns winning contracts, or systematically remove competition. In every case, it's the organization that pays more than it should.

Closely related to bid rigging, price fixing is a collusive scheme where competing suppliers coordinate their bids to artificially inflate costs, deciding in advance who will win the contract and at what price, eliminating any genuine competition from the process.

This scheme occurs after a contract is won. The contractor swaps the promised goods or products for cheaper alternatives and pockets the difference. Substitute goods may be substandard, uncertified, or falsely certified. This kind of scheme can end up being extra costly if the business or government agency in question needs to replace the faulty products or repair damage done by them. Beyond the financial cost, this can have serious real-world consequences when it involves medical devices, construction materials, or other products where quality directly affects safety.

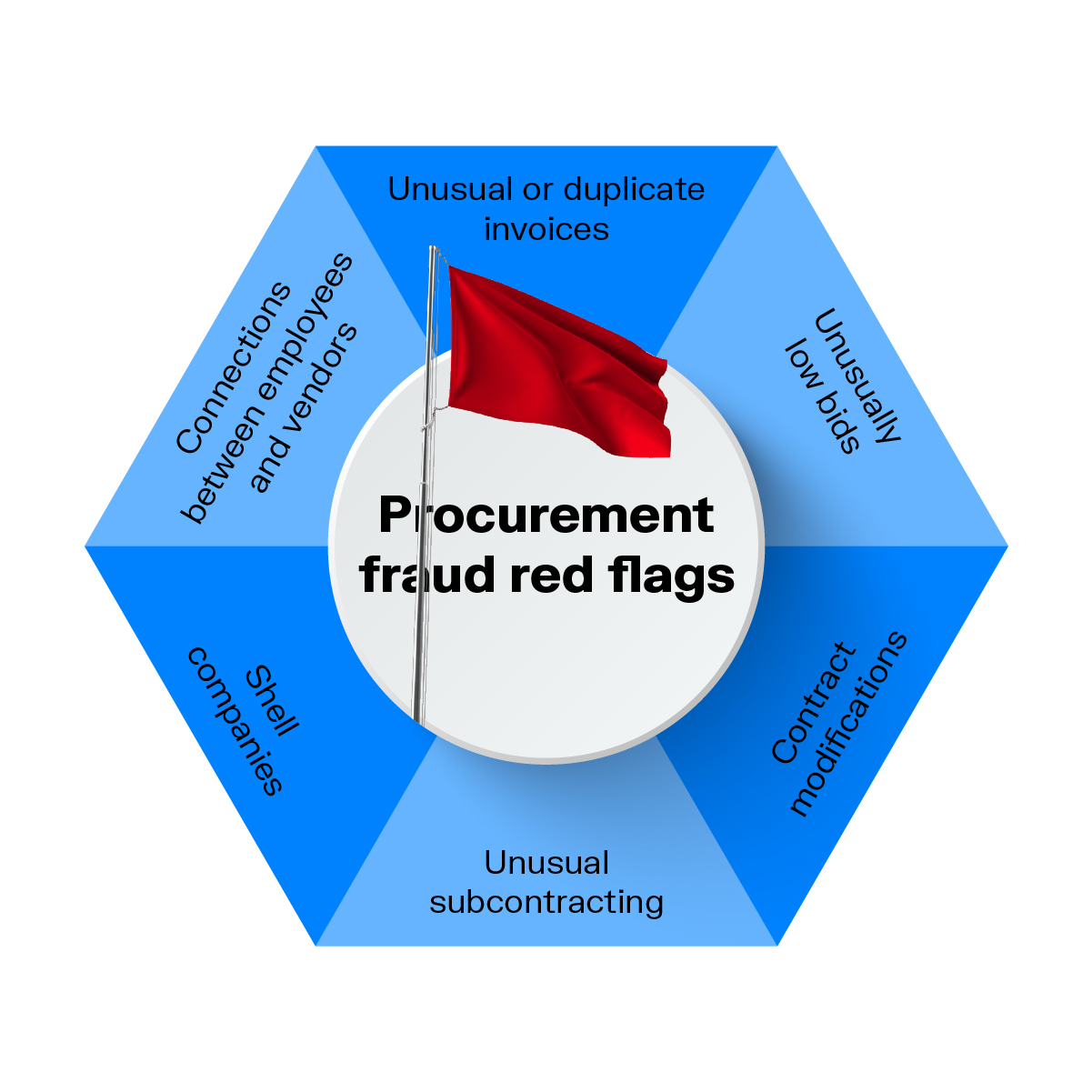

A first step to detecting and effectively investigating procurement fraud is knowing how to spot the red flags. Here are some common ones to look out for.

Corrupt suppliers may create extra invoices or issue invoices for inflated amounts, sometimes with the collusion of an internal employee.

One bid that is obviously lower than the rest could signal that the vendor plans to recoup the difference through product substitution or other post-award fraud. A late bid that is also suspiciously low is worth extra scrutiny, as it may indicate the vendor had access to insider information to position themselves at an advantage.

An employee-vendor relationship is not automatically suspicious, but it becomes a serious problem when it goes undisclosed. A personal, financial, or familial connection that isn't declared can compromise the entire bidding process.

Contracts that are amended repeatedly, especially when those changes increase costs, can indicate that the original terms were manipulated or that fraud is being introduced after the fact.

If a prime contractor is consistently subcontracting large portions of work to specific companies, particularly ones with limited visibility, it warrants a closer look.

Two related but distinct red flags. A shell company is typically an external entity, a vendor with little to no online presence, no physical address, or a newly registered business appearing in competitive bids. A ghost vendor is an internal creation: an employee sets up a fictitious supplier account within the organization's own systems and routes payments to themselves. Both are common covers for procurement fraud and financial crime, and both warrant investigation the moment something about the vendor relationship doesn't add up.

Procurement fraud is difficult to detect for several compounding reasons. Part or all of a scheme may be kept off the books and not immediately visible in standard reporting. Bad actors work hard to conceal the personal relationships, financial interests, and shared connections that would give them away. And siloed data within large organizations gives fraudsters room to operate across departments or systems without anyone seeing the full picture.

This is where many investigations stall. Auditors and investigators are forced to connect information manually across disconnected systems, a process that is slow, resource-intensive, and prone to gaps.

Graph analytics, sometimes called network analytics, addresses all of these challenges directly. Unlike traditional tools that treat data points in isolation, graph technology structures data around nodes (individual entities like employees, vendors, or invoices) and edges (the relationships between them), making it possible to see how everything connects and to query those connections at speed.

By pulling together data from across the organization into one unified view, graph technology closes the gaps that fragmented systems leave open, making it much harder for schemes to stay hidden simply because the relevant information was never in the same place at the same time.

Adding a visualization layer through a platform like Linkurious Enterprise takes this further, letting investigators explore connections interactively in just a few clicks rather than running complex manual queries.

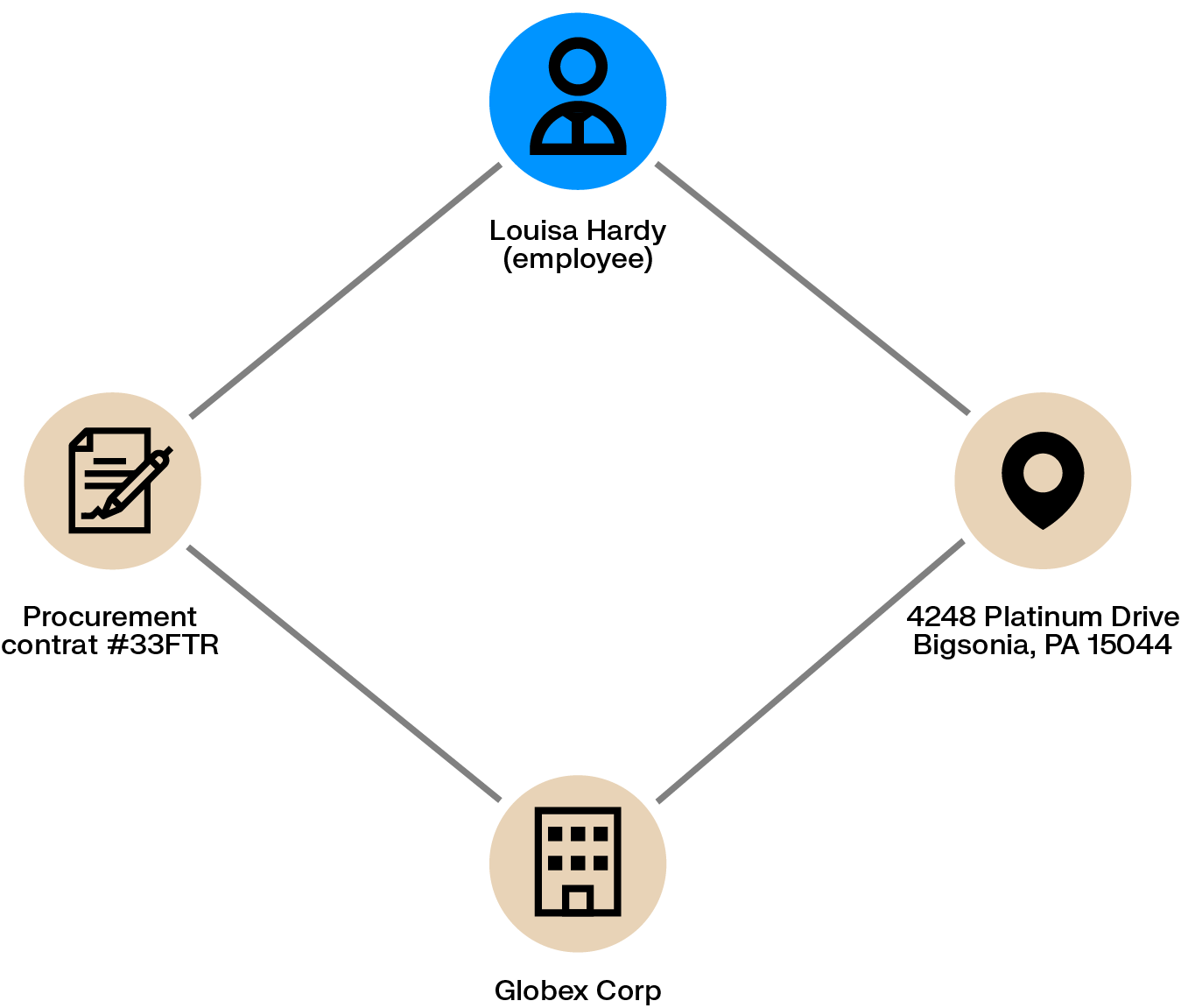

In procurement fraud cases, the connections between entities - employees, vendors, invoices, etc. - are often the evidence. Graph technology makes those connections visible immediately.

An investigator can see at a glance whether an employee shares an address with a vendor making a bid on a contract they oversee. Social media data can be pulled in to surface personal relationships that wouldn't appear in internal records. Ownership data, where available, can reveal whether an employee holds a financial stake in a supplier they are evaluating.

Graph analytics is equally effective for spotting anomalies in invoicing patterns. A cluster of invoices all issued on the same date, an unusual volume of small payments where large ones are typical, or payments to a vendor that spike without a corresponding change in contracted scope: all of these stand out clearly once the data is connected and visualized. By giving investigators this kind of contextual view, graph analytics turns a slow, manual process into something that can move at the speed an investigation actually requires.

Procurement fraud is one of many complex fraud types where graph analytics delivers a meaningful advantage. To see how network analytics can improve fraud detection and investigation across the board, take a look at our in-depth ebook.

A spotlight on graph technology directly in your inbox.